Insuring a Luxury Watch Collection: The 2026 Collector’s Guide to Total Protection

Posted by Luxury of Watches on 9th Jul 2026

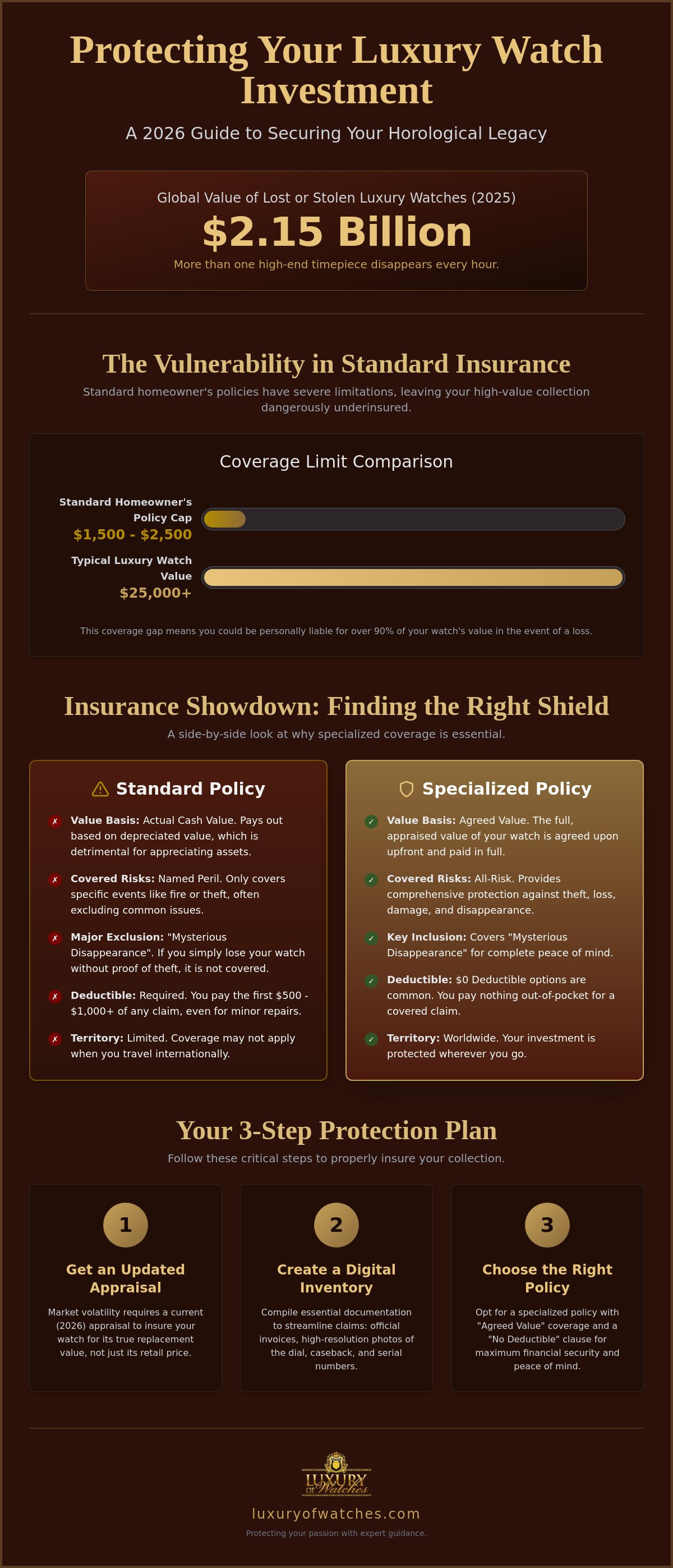

Did you know that the total value of luxury watches reported lost or stolen globally reached a record $2.15 billion in 2025? With more than one high-end timepiece disappearing every hour, the emotional and financial stakes of protecting your luxury watch investment have never been higher. You've likely spent years curating a collection that reflects your personal taste and professional success. It's completely natural to feel a sense of hesitation when wearing a Patek Philippe or a Rolex Cosmograph Daytona in public, especially when standard homeowner's policies often cap jewelry coverage at a mere $2,500. This is a figure that rarely covers high-value assets like those from Javda Jewelry.

This guide provides the clarity you need to move from anxiety to absolute confidence. You'll learn how to navigate the complexities of 2026 market valuations and secure a policy that actually reflects the true replacement cost of your horological legacy. We'll explore the essential documentation required for specialized insurance, the critical difference between retail and market value, and how to establish a verification trail that simplifies the claims process from the moment of acquisition.

Key Takeaways

- Understand why standard homeowner's insurance limits are often insufficient and how specialized policies protect against risks like "mysterious disappearance."

- Learn why the market volatility of 2026 requires updated appraisals to ensure you are protecting your luxury watch investment at its true replacement value.

- Discover the critical documentation needed, from official invoices to high-resolution photography, to create a digital inventory that streamlines future claims.

- Evaluate the financial benefits of "no deductible" specialized coverage, which provides complete peace of mind for those who wear their high-value pieces daily.

- See how acquiring timepieces from trusted sources that offer absolute verification and long-term warranties can lower the risk profile of your entire collection.

Why Your Homeowners Policy Likely Leaves Your Watch Collection Vulnerable

Many collectors assume their standard homeowners or renters policy provides a comprehensive safety net for their entire estate. This assumption is often a costly error. When protecting your luxury watch investment, relying on a general policy is similar to using a simple padlock to secure a bank vault. Standard insurance is designed for the average consumer, not the horological enthusiast whose single timepiece might exceed the value of a luxury vehicle.

The primary issue lies in the "Special Limits of Liability" clause found in almost every standard policy. These clauses restrict coverage for jewelry and watches to a total amount that typically ranges from $1,500 to $2,500. If you own a modern Rolex or a Cartier, these limits won't even cover a fraction of the replacement cost. As market prices for iconic models continue to climb in 2026, these static sub-limits become increasingly dangerous for your financial security.

The Sub-Limit Trap

Standard policies are often blind to the realities of the secondary market. While your home insurance might cover your furniture for its full value, it treats a Patek Philippe the same way it treats a generic wedding band. Inflation and the recent 2026 price increases from major manufacturers mean that even "generous" standard limits are now obsolete. A Scheduled Personal Property rider is a specific policy amendment that lists individual timepieces for their full appraised value to bypass these restrictive sub-limits.

Coverage Gaps: Theft vs. Loss vs. Damage

Most general policies are "named peril" contracts. This means they only pay out if the loss is caused by a specific event listed in the document, such as fire or documented theft. They frequently exclude "mysterious disappearance," which occurs when a watch is lost without evidence of a crime. For a global traveler, the risk of a spring bar failing or a watch being misplaced in a hotel is significant. Understanding the nuances of specialized vs. general insurance is vital for ensuring all-risk protection that follows you across borders.

Beyond simple loss, you must consider the distinction between Actual Cash Value and Replacement Cost. Actual Cash Value policies subtract depreciation from your payout, which is a disastrous formula for timepieces that appreciate over time. To truly succeed in protecting your luxury watch investment, you must secure a policy that pays the full Replacement Cost. This ensures your payout reflects 2026 market rates, allowing you to acquire a comparable model without out-of-pocket expenses. Specialized policies also tend to offer coverage for accidental damage, protecting the intricate mechanical movements that general insurers often ignore.

Specialized vs. General Insurance: Finding the Right Shield

Once you recognize the limitations of a standard homeowners policy, the next decision involves selecting the specific type of coverage that fits your lifestyle. For many, the choice boils down to a dedicated specialized watch insurance provider or a high-value rider through an existing insurer. Each path offers distinct advantages, but the nuances of protecting your luxury watch investment often favor the specialist when dealing with high-volatility brands like Rolex or Patek Philippe.

Specialized insurers understand that enthusiasts don't just store their pieces; they wear them. This is where the "No Deductible" advantage becomes paramount. If you wear a robust Breitling as a daily driver, the risk of accidental damage is statistically higher. A specialized policy often covers these repairs with zero out-of-pocket cost, whereas a traditional rider might require a $500 or $1,000 deductible before the insurer contributes a cent. These specialists also provide worldwide coverage as a standard feature, ensuring your timepiece is protected from the moment you clear customs to the moment you return home.

Comparing Specialized Watch Policies

The most significant benefit of a specialized contract is the shift from Actual Cash Value to Agreed Value. In an Agreed Value contract, you and the insurer settle on a fixed payout amount based on a current appraisal. This eliminates the uncertainty during a claim. Many modern digital-first insurers even offer automatic inflation protection, which can increase your coverage by a set percentage annually to keep pace with the 2026 price hikes seen across the industry. Because these providers focus solely on jewelry and horology, their claims adjusters are often more knowledgeable about the specific nuances of vintage components and brand-specific service requirements.

The Traditional Rider: When It Makes Sense

A traditional "scheduled personal property" rider attached to your homeowners policy can be an efficient option if you only own one or two pieces. Insurers often offer bundling discounts that make the premium highly competitive. However, collectors should be wary of the potential for a "claim spike." Filing a claim for a stolen watch through your homeowners insurance could lead to a significant increase in your entire home and auto premiums. Additionally, traditional insurers almost always require a formal, written appraisal for every item, regardless of value. When you acquire pre-owned luxury watches from a reputable source, ensure you receive the detailed documentation and verification needed to satisfy these rigorous underwriting requirements without delay.

Appraisals and Market Value: Accurate Valuation in 2026

The luxury watch market is currently characterized by rapid price shifts and high demand for iconic steel models. This environment makes the task of protecting your luxury watch investment a dynamic process rather than a one-time event. To ensure your collection is fully covered, you must understand the distinction between three critical figures: Manufacturer’s Suggested Retail Price (MSRP), Secondary Market Value, and Replacement Cost. In 2026, these numbers rarely align. While MSRP is the price set by the brand, Replacement Cost is the amount an insurer pays to help you acquire the same watch at current market rates, which often includes a significant premium.

Relying on a valuation from even a few years ago is a significant risk. For instance, a 2023 appraisal for a Rolex Submariner is dangerously outdated in today's market. With Rolex implementing price increases in early 2026, a white-gold Cosmograph Daytona now retails for $56,400, up from $51,800 just a year prior. If your policy is tied to an old appraisal, you'll be forced to cover the thousands of dollars in difference yourself. A sales receipt serves as proof of what you paid, but only a professional appraisal provides the documented evidence of current value that an underwriter requires for a high-value claim.

The Volatility Factor: Rolex and Patek Philippe

High-demand brands like Rolex and Patek Philippe require "Agreed Value" policies because their secondary market prices often dwarf their retail counterparts. The Patek Philippe index has climbed 18% over the last year, while the Rolex index rose 9%. To stay ahead of these fluctuations, collectors should follow the two-year rule, which suggests updating appraisals every 24 months for high-volatility pieces. For insurance purposes, Retail Replacement Value represents the cost to buy the item new from a dealer, while Fair Market Value is the price the watch would fetch in a sale between a willing buyer and seller in its current condition.

Insuring Pre-Owned and Vintage Watches

Valuing a pre-owned luxury watch or a vintage model presents unique challenges. Without a current MSRP for discontinued references, appraisers must establish a value baseline using recent auction results and private sales data. When protecting your luxury watch investment, the presence of original parts and a documented service history can swing a valuation by thousands of dollars. Insurers look for absolute verification of authenticity, which is why acquiring pieces from sources that provide official documentation and long-term warranties is essential for a smooth underwriting process. If you own New Old Stock (NOS) pieces, ensure your appraiser notes their pristine, unworn condition to justify a higher replacement ceiling.

The Step-by-Step Guide to Securing Your Watch Policy

Precision defines a great timepiece; it should also define your insurance application. Moving from an outdated general policy to a specialized contract requires a methodical approach to ensure no gaps remain in your coverage. Protecting your luxury watch investment is a multi-stage process that begins long before you sign the final paperwork. By following a structured roadmap, you'll create a robust defense that simplifies the claims process and ensures your horological legacy remains secure.

The first stage involves meticulous inventory management. You must create a digital "Watch Box" that includes the exact serial numbers, reference numbers, and high-resolution imagery for every piece. This data acts as your primary proof of possession. Once your inventory is set, gather all supporting documentation. This includes original invoices, warranty cards, and certificates of authenticity. When you acquire a timepiece from the curated selection of Men's Luxury Watches at Luxury of Watches, you receive the absolute verification and official documentation necessary to satisfy the most stringent underwriting requirements from the start.

Inventory and Digital Proof

Modern insurers in 2026 have moved beyond simple descriptions. To meet their standards, adopt the "Four-Photo Rule" for every watch in your collection. This involves capturing clear, well-lit images of the dial, the caseback, the serial number engraving, and the "full set" including the box and papers. Store these files in a secure, cloud-based environment to ensure redundancy. Many collectors now include a brief video walkthrough of their collection, which acts as undeniable proof of the condition and existence of the pieces at a specific point in time. This level of detail is becoming a preferred standard for loss adjustors who have seen a 25% increase in claims over the last three years.

After your documentation is prepared, you must choose an underwriter that matches your lifestyle. If you travel frequently, look for policies that offer worldwide coverage without geographical restrictions. During the application, be transparent about your security measures. Disclosing the use of a high-tier home safe or a monitored alarm system can often lead to more favorable terms. Finally, perform a rigorous policy review. Check for "Pairs and Sets" clauses, which are vital if you own a matched set of timepieces, and ensure an "Inflation Guard" is present to account for the market volatility discussed in previous sections.

The Fine Print: Exclusions to Watch For

Success in protecting your luxury watch investment often depends on what the policy does not cover. If you own a large collection, ask about "In-Vault" versus "Out-of-Vault" rates. You can save significantly on premiums by listing pieces you rarely wear as vault-restricted. Be aware that most policies exclude "wear and tear" or internal mechanical breakdowns; these are maintenance issues, not insurance claims. To prevent such issues and keep your automatic pieces in optimal condition, you can visit Aevitas UK for premium storage and winding solutions. However, they should cover external damage like a shattered sapphire crystal or a crushed case. Understanding these Proof of Loss requirements today will prevent frustration if you ever need to file a claim in the future.

The Role of Verification and Trusted Acquisition in Security

The journey of protecting your luxury watch investment does not begin with an insurance quote. It starts at the moment of acquisition. Insurers are fundamentally in the business of risk assessment, and they look favorably upon collectors who source their timepieces from established, reputable intermediaries. When you acquire a piece through a platform like Luxury of Watches, you aren't just buying a watch; you're securing a verified asset with a documented history. This transparent provenance is exactly what an insurance underwriter needs to see to approve a high-value policy without friction.

Absolute verification acts as your primary defense against one of the most frustrating aspects of the insurance world: the claim denial. In the secondary market, "Frankenstein" watches or high-quality clones can lead to an insurer refusing to pay out, citing a lack of authenticity. By providing a paper trail that includes official documentation from the point of sale, you eliminate this ambiguity. Additionally, the 5-year in-house warranty provided by Luxury of Watches serves as a powerful signal of mechanical integrity. It demonstrates to the insurer that the timepiece has been expertly vetted and maintained, reducing the perceived risk of internal failure or undisclosed damage.

Documentation as a Security Asset

Insurers often require more than just a receipt; they require a narrative. The verification process at Luxury of Watches creates a professional paper trail that established insurers trust. This is particularly critical for brands like Cartier, where the presence of the original box and papers (B&P) can significantly influence the insurable value. Keeping these components in pristine condition doesn't just satisfy the collector's desire for a "full set." It provides the insurer with a baseline of value that is much harder to dispute during a claims experience. A secure purchase from a trusted source ensures that if the unthinkable happens, your documentation is as unassailable as the timepiece itself.

Next Steps for the Serious Collector

As you look toward the remainder of 2026, your strategy for protecting your luxury watch investment should be proactive. If you've recently added a high-value piece to your safe, schedule a professional appraisal immediately to capture its current market replacement cost. Market shifts can happen quickly, and your total collection value may have already outpaced your existing policy limits. Review your coverage annually to ensure your horological legacy is never left under-insured. If you are ready to expand your portfolio with a piece that comes with built-in peace of mind, browse our verified collection of Rolex and luxury timepieces to find your next investment-grade watch. Integrating a professional maintenance schedule with your insurance strategy is the final step in ensuring your collection remains as valuable and functional as the day it was manufactured.

Future-Proofing Your Collection for the Years Ahead

The landscape of luxury watch collecting in 2026 demands more than just a keen eye for craftsmanship; it requires a disciplined approach to risk management. As we've explored, standard homeowners policies often fall short of providing the coverage necessary for high-volatility brands. By shifting toward specialized insurers and maintaining a rigorous schedule of biennial appraisals, you ensure that your collection remains protected at its true market replacement cost. Protecting your luxury watch investment is ultimately about creating a seamless bridge between acquisition and long-term security.

The foundation of this security is built on absolute verification and expert documentation. At Luxury of Watches, we provide the rigorous authentication and official paperwork required to satisfy even the most discerning insurance underwriters. Every timepiece in our collection comes with a 5-year in-house warranty, offering a level of mechanical reassurance that is rare in the secondary market. When you're ready to expand your portfolio with confidence, Secure Your Next Investment at Luxury of Watches. Your passion for horology deserves a protection strategy as precise as the movements you admire.

Frequently Asked Questions

Do I need an appraisal to insure my watch?

Yes, you generally need a professional appraisal to secure a scheduled policy or an agreed-value contract. While some modern digital insurers waive this requirement for pieces below a specific value threshold, high-tier timepieces from manufacturers like Patek Philippe or Audemars Piguet almost always require documented valuation. This ensures your coverage reflects the 2026 market reality rather than an outdated retail price, providing a clear baseline for any future claims.

Does watch insurance cover accidental damage, like a cracked crystal?

Specialized watch insurance policies typically cover accidental damage, including shattered sapphire crystals, bent lugs, or crushed cases. This is a significant advantage over standard homeowners insurance, which often limits coverage to specific named perils like fire or theft. Comprehensive protection ensures your daily wearer is covered against the common hazards of an active lifestyle, allowing you to wear your high-value pieces with absolute confidence in any environment.

Will my insurance pay the current market price if my watch is stolen?

Your payout depends entirely on whether you have an Agreed Value policy supported by a recent appraisal. If your contract is based on a current valuation, the insurer will pay the stated amount to cover the market price. However, if you rely on a 2023 valuation for a Rolex Submariner, you'll likely face a significant financial shortfall due to the price appreciation seen across the industry in early 2026.

Is my watch covered when I travel internationally?

Most specialized policies provide worldwide coverage as a standard feature, protecting your collection across international borders wherever you go. This is essential for the global collector who travels frequently for business or leisure. Standard homeowners policies may restrict coverage once you leave your primary residence or apply much lower sub-limits to items lost or stolen while traveling abroad. Always verify the geographic scope of your specific policy before departing.

What is the average cost of luxury watch insurance per year?

The typical annual cost for insuring a luxury timepiece is between 1% and 2% of its appraised value. For collectors with assets valued over $100,000, these rates often decrease to between 0.5% and 1.5% depending on the provider. This modest premium is a small price to pay for the peace of mind that comes with protecting your luxury watch investment against the rising rates of global watch theft.

Does a watch warranty count as insurance?

No, a watch warranty and an insurance policy serve two completely different purposes for a collector. A warranty, like the 5-year in-house warranty provided by Luxury of Watches, protects against mechanical failures and internal defects in the movement. Insurance is designed to cover external events such as theft, accidental loss, or physical damage caused by outside forces. You truly need both to ensure your collection is fully protected.

What happens if I lose my watch but don’t have the original receipt?

While a receipt is helpful, it isn't the only way to prove ownership to an insurance company. A professional appraisal combined with clear photography of the watch and its serial number is often sufficient for a claim. This is why maintaining a comprehensive digital inventory is a critical step in protecting your luxury watch investment. Cloud-based storage ensures your records are accessible even if your physical documentation is lost or destroyed.

Can I insure a watch I bought on the secondary market?

Absolutely, watches acquired on the secondary market are fully insurable as long as you can prove authenticity. The key is establishing the current replacement value through a qualified appraiser who understands the nuances of the pre-owned market. Purchasing from a reputable source that provides absolute verification and official documentation makes the insurance application process much faster, as underwriters trust the established provenance and mechanical integrity of the piece.